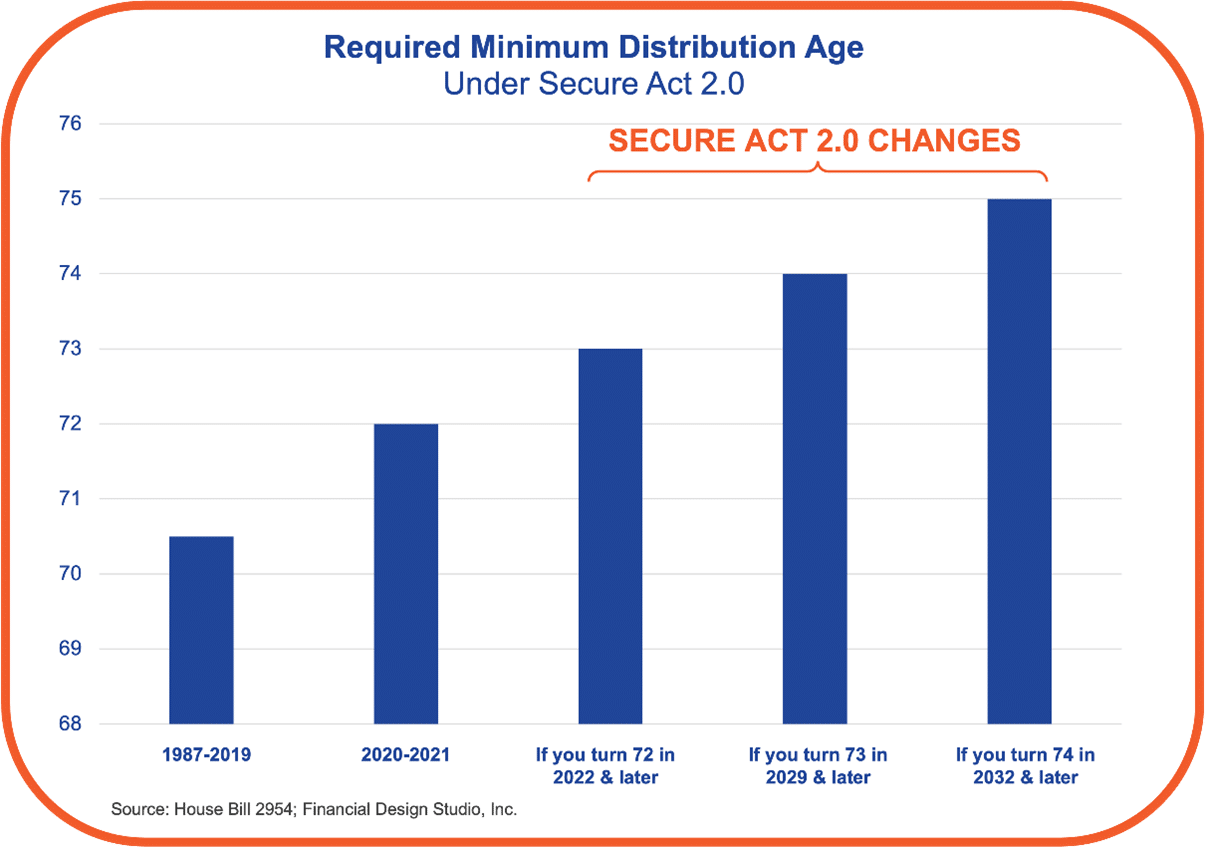

RPOA Retirement Planner Shawn Stone, CRPC®, explains some of these changes, “For those who are over the age of 73 as of 2023, you must take RMDs from retirement accounts like employer-sponsored retirement plans or IRAs by December 31, 2023. Failure to do so could result in a hefty 50% penalty by the IRS on the RMD amount, but as of January 2023, this penalty can be dropped if the RMD is taken by the end of the following year for missed payments.”

Taxes apply differently to various types of investment accounts. For example, IRAs, 401(k)s and some other types of accounts are tax deductible at the front end. These are beneficial accumulation vehicles because they allow your money to grow without being taxed until you make withdrawals. But according to Ken Moraif, Founder and CEO of RPOA, “I always recommend planning your pre-tax account distributions with your tax burden in mind. Money withdrawn from those accounts can be considered ordinary income, which often incurs the highest tax. We recommend consulting a tax professional or your financial planner to ensure all is being done properly as unwinding improper contributions can create a lot of problems and extra work.”

“A traditional IRA lowers your total taxable income because contributions are made pre-tax,” Stone emphasizes, “No matter whether you itemize or take the standard deduction, your income taxes can be lower when utilizing pre-tax contributions. Depending on your income level, Roth IRAs can be a useful tool to invest in before your retire to help ease your tax bill in your golden years because those withdrawals won’t affect your income bracket when you take them down the road.”

At RPOA, our goal is for your money last as long as you do and for you to have financial peace of mind. Staying informed on any legislative changes that may affect your retirement, including changes to Social Security, Medicare, and taxes, we believe are integral to keeping your plan for retirement on track.

Want help getting a retirement plan together that works for you and your needs, please reach out to talk with one of our retirement planners to learn more.