You’ve probably heard that rebalancing your portfolio is a good practice, but do you know why you should do it? It’s actually a strategy to help to control risk—and one I believe is especially important for retired investors.

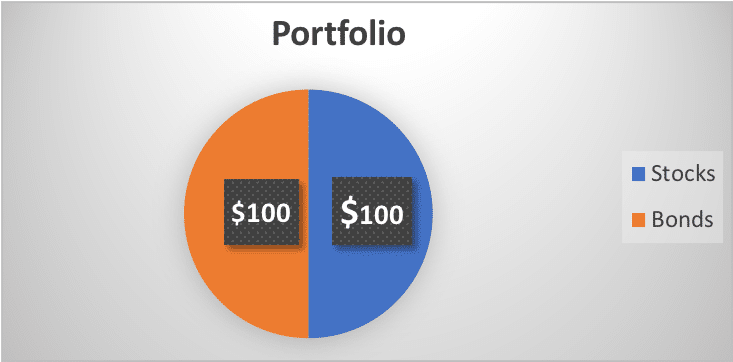

Let me illustrate how it works: Let’s say you have $200. You’ve figured out your risk profile, and decide you want a 50/50 stocks/bonds portfolio.

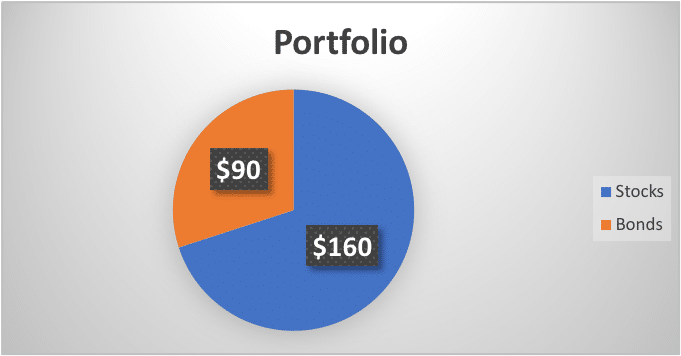

In our imaginary world, your stocks do extremely well, going up 60%. It’s not such a stretch: this has happened in the real world multiple times over the last few decades. Emerging markets, real estate, and tech stocks all rose significantly in short periods of time.

Back to our example: At the same time your stocks rose, your bonds did terribly, losing 10 percent. So now you have $160 in stock and $90 in bonds.

Let’s examine what happened. Though your bonds lost 10%, your stocks gained 60%, and your $200 is now $250. You made 25% on your investment. Life is good, right?

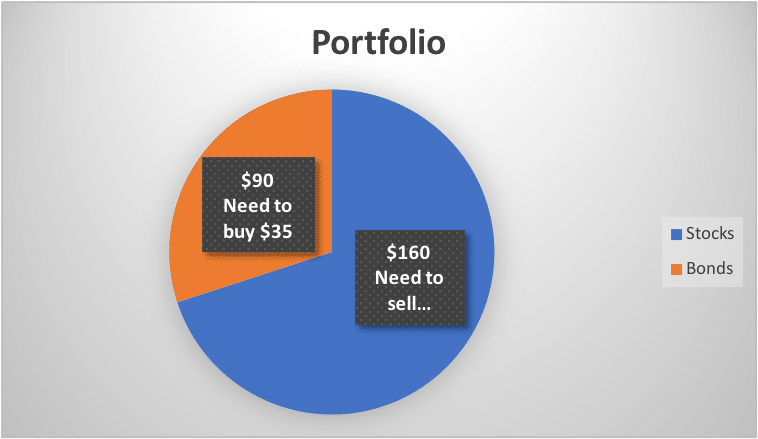

But now you have a problem. Your 50/50 portfolio morphed into a 70/30 portfolio. If you decided 50/50 is the right amount of risk for you, your portfolio is now riskier than is appropriate. And historically, investments that rose dramatically often drop shortly afterward; and the ones that lost money often go up. In other words, 70% of your investments will probably fall and 30% percent will probably rise.

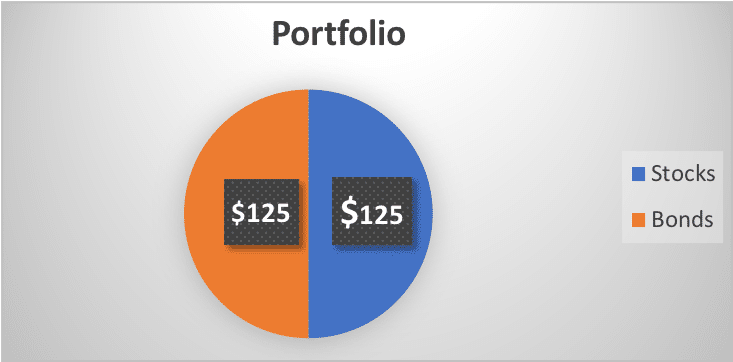

Time to rebalance. To get back to 50/50, you need to sell $35 worth of stocks and buy $35 worth of bonds, so your $250 is evenly split.

In this example, what did rebalancing your portfolio do for you—and how could it benefit you in the real world? As I mentioned earlier, it seeks to help control risk. Your stocks could go up again to the point where 90% of your investments were in stocks. Think about people who had 90% of their money invested in tech stocks during the dot-com bubble. When tech failed 90%, those investors lost 90% on 90% percent of their money, which was 81% percent of their investments. Imagine losing that much money when you are living on your retirement investments. How long could you live on 19% of your money? By rebalancing your portfolio, you are mitigating that type of situation.

Secondly, think about how you bought and sold while rebalancing. You bought low and sold high: the obvious preferred trading method.

I think even this simple example demonstrates the value of rebalancing your portfolio (and its extra importance to retired investors). We regularly rebalance our clients’ portfolios at RPOA and we’d love to talk to you about it, too. We can also discuss your entire retirement plan: how much money you have, where you’re invested, and potential Social Security and income tax strategies—all at no charge or obligation. Contact us today.

Ken Moraif, CFP®, MBA

Senior Advisor at Retirement Planners of America