By Shawn Stone

A big question on seniors’ minds earlier this year was: How much of a e Social Security increase is coming in 2023?

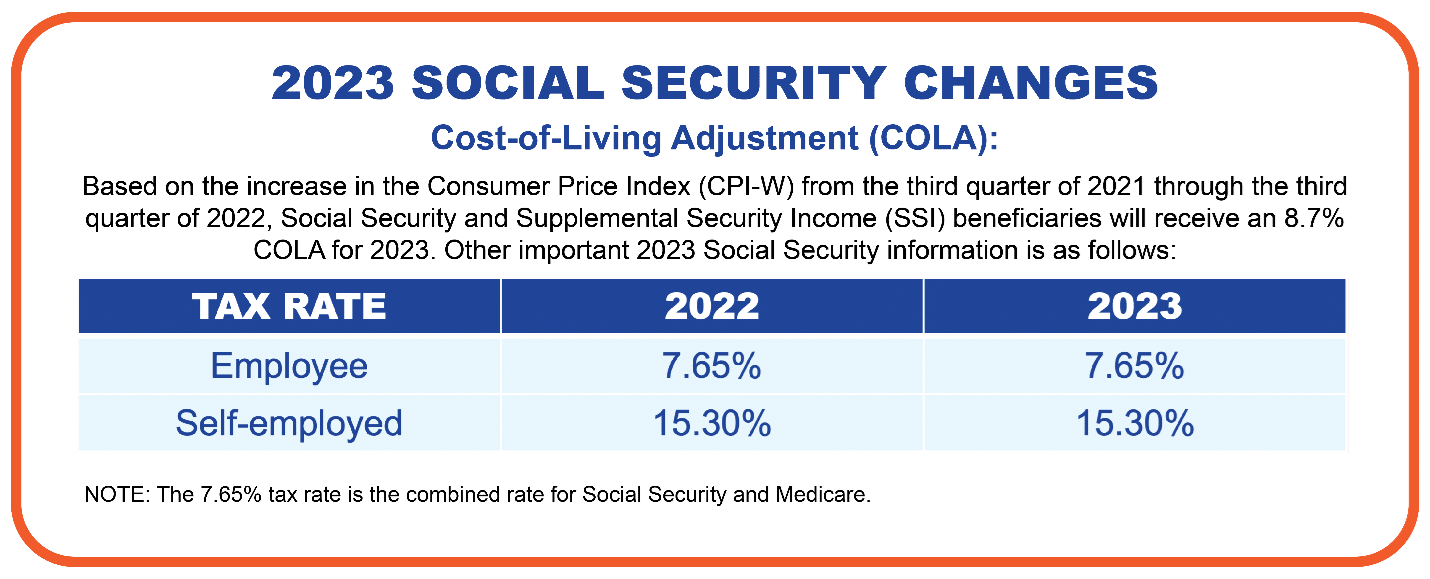

By mid-October, they had their answer. In 2023, Social Security benefits will be eligible for an 8.7% cost-of-living adjustment (COLA) based on third quarter inflation data. Social Security hasn’t seen a raise like that in decades.

However, will an increase of 8.7% actually increase the purchasing power of Social Security beneficiaries?

Source: ssa.gov

COLA increases are intended to offset the decline in value of the dollar. The dollar’s purchasing power has been significantly impacted by inflation, and COLA is meant to restore that power. In other words, the goal is to make your dollar worth a dollar again if it is now worth 92 cents.

As a result of COLA, retirees on Social Security will receive an increase, but considering the rising cost of things like healthcare and other life essentials, I do not believe it is advisable to view it as a ‘raise’. These adjustments were not intended as a raise. They were justified by high inflation, which has increased the cost of living. Keeping up with inflation isn’t a raise; it’s keeping your dollar in line with inflation.

Those taking Social Security benefits will see an increase in their benefits, but their pensions and investments may not. Seniors may not come out ahead financially in the New Year since what they gain in a higher monthly benefit may be offset by higher expenses over time. For example, like last year, increases in other costs may offset Medicare costs in the future.

The good news for seniors is that their 8.7% Social Security COLA could be a financial gain if inflation levels start to wane. The Consumer Price Index (CPI), which measures changes in consumer prices, only rose 7.7% in September — the lowest CPI increase in many months. CPI and other inflation reports may be signaling that inflation has peaked.

By locking in a higher COLA based on a higher level of annual inflation, seniors may gain some purchasing power in the long run if inflation wanes. I believe that type of increase would likely be modest, though.

In my view, a COLA of 8.7% next year appears to have a chance of holding up, but it’s too early to tell. Some Americans are skeptical that an increase that large will improve their financial situation.

I believe the most important takeaway here is that COLA is just making up for lost the loss in value of the dollar. Spending more money doesn’t necessarily mean saving more. This is meant to compensate for the loss of purchasing power — and I believe keeping your spending to a minimum will help you have a better chance of achieving this.

For those entering retirement or already there, I think you should be aware of the changes that may occur month-to-month or year-by-year that impact your whole financial picture. Neither COLA nor inflation will remain constant. COLA may increase, but your budget may also rise with inflation, so COLA may not be enough to keep up. As inflation remains elevated, I think it should be a factor in your retirement planning process.

At Retirement Planners of America, we want you to have confidence and financial peace of mind in retirement. If you’d like to meet with a member of our team to learn more, visit our website here.